Investment firms include private equity funds (which raise capital to invest in start-ups or existing businesses) and hedge funds (investment funds that specialize in certain investments such as debt instruments, stocks or derivatives). They are typically not organized as public corporations, with stocks traded on an exchange, but as partnerships.

Instead of shares of stock, partners own a percentage of the firm. Although all the partners hold an ownership share, there are general partners who manage the business and may receive additional shares to compensate them. This additional compensation is called carried interest.

Instead of shares of stock, partners own a percentage of the firm. Although all the partners hold an ownership share, there are general partners who manage the business and may receive additional shares to compensate them. This additional compensation is called carried interest.

Congress is debating a bill that would tax carried interest at higher rates. However, raising the tax rate on carried interest will not result in any net gain to the U.S. Treasury, but it will have negative impacts on productivity, wages and the cost of investment.

How Carried Interest Is Taxed. When the general partners of an investment firm are paid a flat fee for their management services, it is considered earned income and taxed at ordinary income tax rates. Often, however, general partners receive as payment a portion of the partnership that was funded by the limited partners (those who contributed the capital to fund the firm); the income from that transferred ownership share is called carried interest, and it is taxed based on its form:

- If it is a distribution of interest from an investment by the partnership, the carried interest is taxed as ordinary income (currently up to 35 percent but due to rise to 39.6 percent next year).

- If it is a distribution of dividends earned by the partnership, it is taxed up to 15 percent (due to rise to 39.6 percent next year).

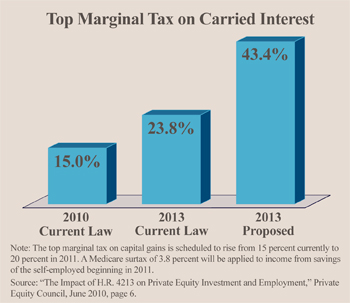

- If it is capital gains – the increase in the value of an asset – it is taxed at the current capital gains rate of 15 percent (due to increase to 20 percent next year).

- Moreover, beginning in 2013, all income from savings, whether taxed at the income tax or the capital gains tax rate, will be subject an additional 3.8 percent Medicare tax for individuals earning more than $200,000 a year.

The House version of the bill required capital gains distributions to be treated as 75 percent ordinary income in 2013 (50 percent in 2011 and 2012), meaning only 25 percent of carried interest would be eligible for the more favorable capital gains rate. A Senate amendment to the House bill would lower the percentages treated as ordinary income to 45 percent in 2011 and 65 percent in 2014.

The Senate version of the bill would require general partners to treat a portion of the carried interest as ordinary income only to the extent that their share of the partnership was not due to investment of their own money (general partners may also contribute some of the capital), but rather is compensation for their services to the partnership.

Effect on Tax Revenues. For the most part, it makes no difference in federal tax revenues whether payments to the general partner take the form of a fee or a portion of the partnership returns. Consider a case in which the partnership earns capital gains and the general partner gets part of the total:

- The Treasury will collect an amount equal to the total capital gains income times the capital gains tax rate. (For instance, $1,000 multiplied by the 15 percent capital gains rate equals $150 in tax revenue.)

- It will collect some from the limited partners and some from the general partners – the split does not affect the total revenue ($150).

Then consider an alternative to carried interest in which the partnership pays the general partner a management fee high enough to compensate for the higher tax rate on the general partner, and the limited partners keep and pay tax on the entire $1,000 capital gains:

- The general partner would pay ordinary income tax rates on their fee. (For example, 35 percent on a fee of $100 equals $35.)

- But the limited partners would get a tax deduction for the management fee that they could claim against ordinary income.

- The tax they save with the deduction of the management fee would equal the tax paid on the fee by the general partners ($35), resulting in zero net revenue to the Treasury.

The Treasury would only receive the tax on the capital gains earned by the partnership. In other words, if carried interest were treated as ordinary income, and replaced by fees, the Treasury would net no additional income.

Carried Interest and Charities. Some limited partners are tax-exempt institutions, such as schools and charities. They would not be able to write off their portion of the augmented management fee as a tax deduction. As a result, the Treasury would receive increased tax revenues equal to the difference between the ordinary income tax rate and the capital gains tax rate on the portion of the general partner's fee paid by the tax-exempt partners. The tax-exempt groups would experience corresponding reductions in their net earnings from the partnership. In effect, treating carried interest as ordinary income taxes tax-exempt entities.

Conclusion. If carried interest is treated as ordinary income, it would net the Treasury little additional income. Any revenue gain would be largely at the expense of charities and schools. Linking the returns of the management to the performance of the investments via carried interest is a strong motivator for general partners to make investments as productive as possible. Breaking that link by raising taxes on carried interest would reduce these incentives, and force more of the investment risk onto the limited partners. To the extent that additional revenues were raised by taxing carried interest at higher rates, it would raise the cost of investment, as well as reduce productivity and wages.

Stephen J. Entin is president and executive director of the Institute for Research on the Economics of Taxation in Washington, D.C.